id age gender hr sysbp diasbp bmi cvd afb sho chf av3 miord mitype year

1 1 83 0 89 152 78 25.54051 1 1 0 0 0 1 0 1

2 2 49 0 84 120 60 24.02398 1 0 0 0 0 0 1 1

3 3 70 1 83 147 88 22.14290 0 0 0 0 0 0 1 1

4 4 70 0 65 123 76 26.63187 1 0 0 1 0 0 1 1

5 5 70 0 63 135 85 24.41255 1 0 0 0 0 0 1 1

6 6 70 0 76 83 54 23.24236 1 0 0 0 1 0 0 1

admitdate disdate fdate los dstat lenfol fstat

1 01/13/1997 01/18/1997 12/31/2002 5 0 2178 0

2 01/19/1997 01/24/1997 12/31/2002 5 0 2172 0

3 01/01/1997 01/06/1997 12/31/2002 5 0 2190 0

4 02/17/1997 02/27/1997 12/11/1997 10 0 297 1

5 03/01/1997 03/07/1997 12/31/2002 6 0 2131 0

6 03/11/1997 03/12/1997 03/12/1997 1 1 1 1The lasso model allows you to effectively identify important features in a large regression model. Here is an illustration of how to use a the lasso model with survival data from the Worcester Heart Attack Study.

I’ve followed the glmnet vignette for Cox regression closely. You might find that explanation to be clearer than what I present below.

Description of the whas500 dataset

Here is a brief description of the whas500 dataset, taken from the data dictionary on my github site.

The data represents survival times for a 500 patient subset of data from the Worcester Heart Attack Study. You can find more information about this data set in Chapter 1 of Hosmer, Lemeshow, and May.

Here are the first few rows of data and the last few rows of data. Row 101 needs to be removed.

Here are a few descriptive statistics

gender: gender

gender n

1 0 300

2 1 200

cvd: History of Cardiovascular Disease

cvd n

1 0 125

2 1 375

afb: Atrial Fibrillation

afb n

1 0 422

2 1 78

sho: Cardiogenic Shock

sho n

1 0 478

2 1 22

chf: Congestive Heart Complications

chf n

1 0 345

2 1 155

av3: Complete Heart Block

av3 n

1 0 489

2 1 11

miord: MI Order

miord n

1 0 329

2 1 171

mitype: MI Type

mitype n

1 0 347

2 1 153

year: Cohort Year

year n

1 1 160

2 2 188

3 3 152

dstat: Discharge Status from Hospital

dstat n

1 0 461

2 1 39

fstat: Vital Satus

fstat n

1 0 285

2 1 215age: Age at Admission

age

Min. : 30.00

1st Qu.: 59.00

Median : 72.00

Mean : 69.85

3rd Qu.: 82.00

Max. :104.00

hr: Initial Heart Rate

hr

Min. : 35.00

1st Qu.: 69.00

Median : 85.00

Mean : 87.02

3rd Qu.:100.25

Max. :186.00

sysbp: Initial Systolic Blood Pressure

sysbp

Min. : 57.0

1st Qu.:123.0

Median :141.5

Mean :144.7

3rd Qu.:164.0

Max. :244.0

diasbp: Initial Diastolic Blood Pressure

diasbp

Min. : 6.00

1st Qu.: 63.00

Median : 79.00

Mean : 78.27

3rd Qu.: 91.25

Max. :198.00

bmi: Body Mass Index

bmi

Min. :13.05

1st Qu.:23.22

Median :25.95

Mean :26.61

3rd Qu.:29.39

Max. :44.84

los: Length of Hospital Stay

los

Min. : 0.000

1st Qu.: 3.000

Median : 5.000

Mean : 6.116

3rd Qu.: 7.000

Max. :47.000

lenfol: Follow Up Time

lenfol

Min. : 1.0

1st Qu.: 296.5

Median : 631.5

Mean : 882.4

3rd Qu.:1363.5

Max. :2358.0 Simple analysis

I am going to show the R code from this point onward so you can see the actual programming required to fit a lasso model.

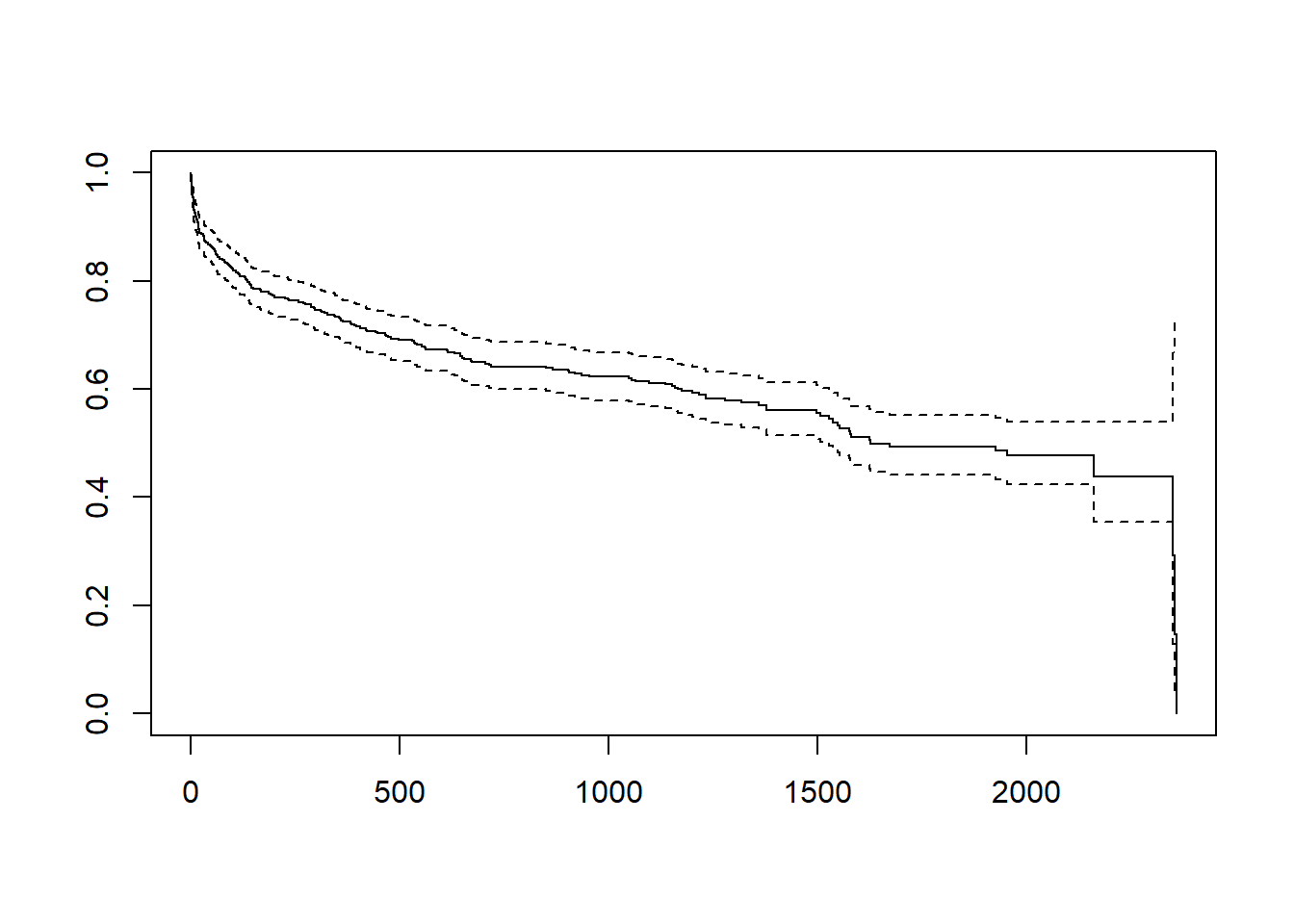

Here is an overall survival curve.

plot(Surv(w1$lenfol, w1$fstat))

Here is the traditional Cox model

simple_fit <- coxph(

Surv(w1$lenfol, w1$fstat) ~

cvd +

afb +

sho +

chf +

av3 +

miord +

mitype,

data=w1)

coef(simple_fit) cvd afb sho chf av3 miord

-0.13512116 0.12295437 1.17397718 1.13970970 0.03502956 0.25505995

mitype

-0.75381851 The lasso model

You can find the lasso regression model in the glmnet package. One important difference with glmnet is that it does not use a formula to define your model. Instead you provide matrices for your dependent variable and your independent variables. In a Cox regression model, the dependent matrix has a column for time and a second column with an indicator variable (1 means the event occurred and 0 means censoring).

ymat <- cbind(w1$lenfol, w1$fstat)

dimnames(ymat)[2] <- list(c("time", "status"))

xmat <- as.matrix(w1[ , 8:14])

dimnames(xmat)[2] <- list(vnames[8:14])

lasso_fit <- glmnet(xmat, ymat, family="cox", standardize=FALSE)

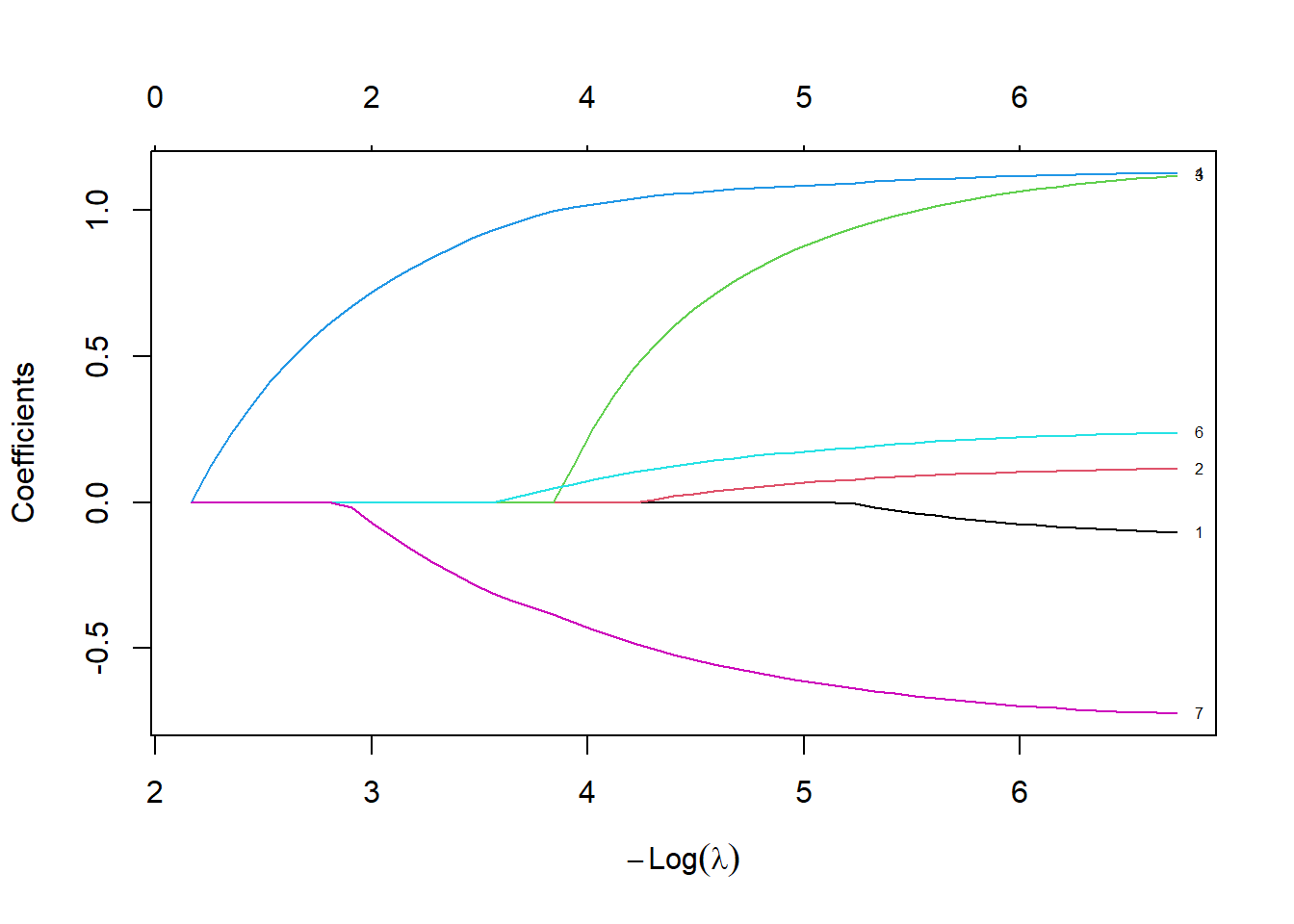

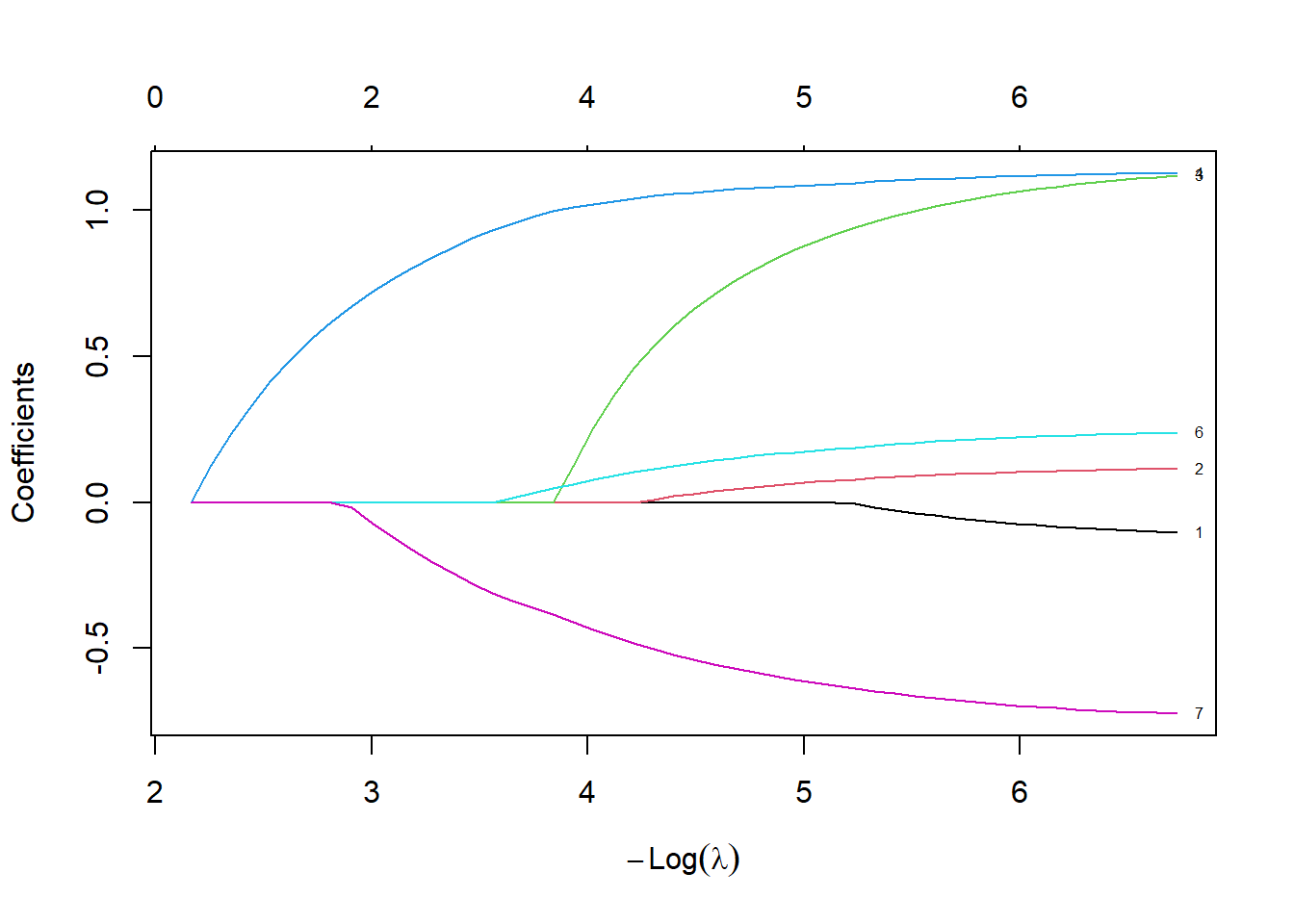

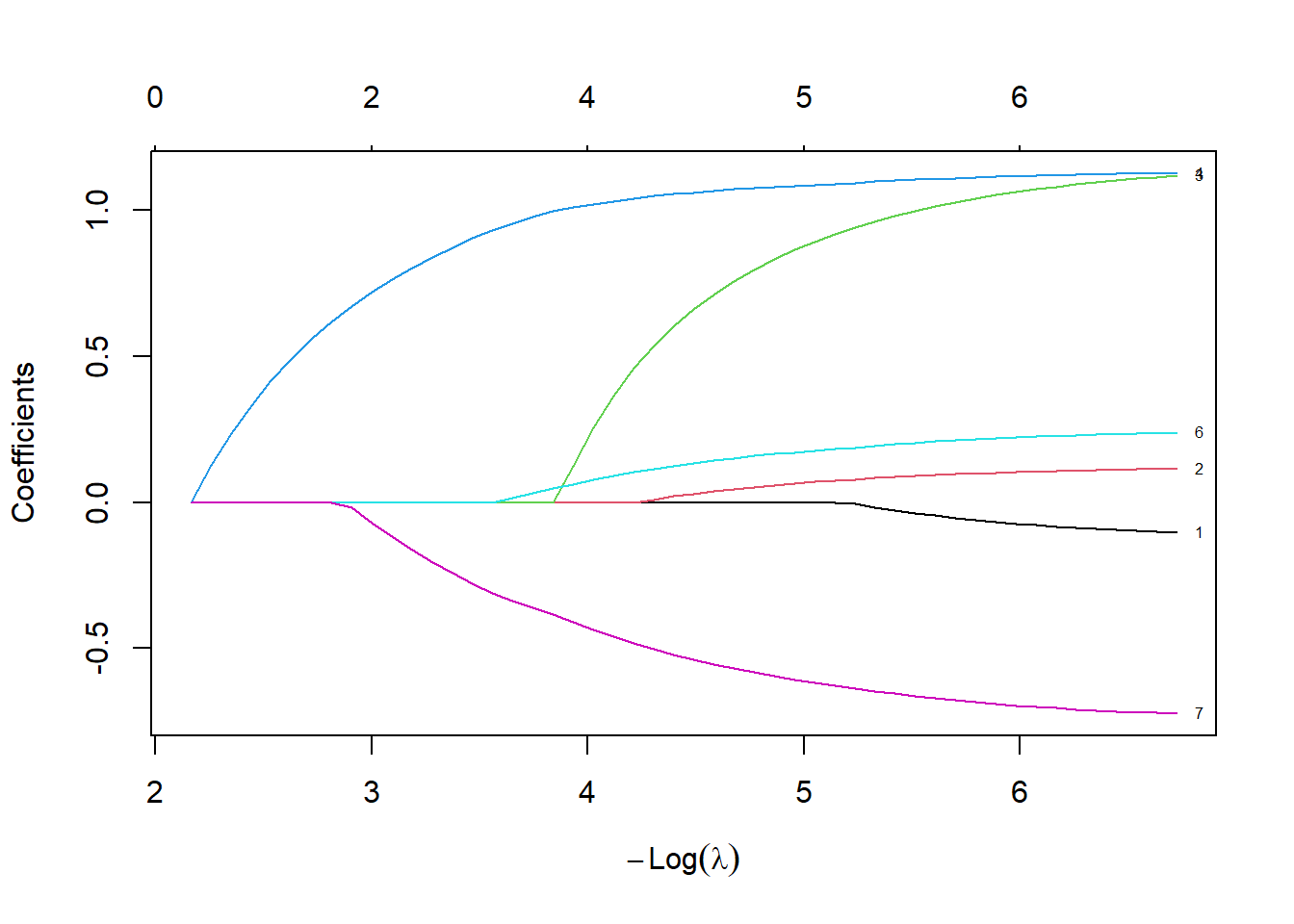

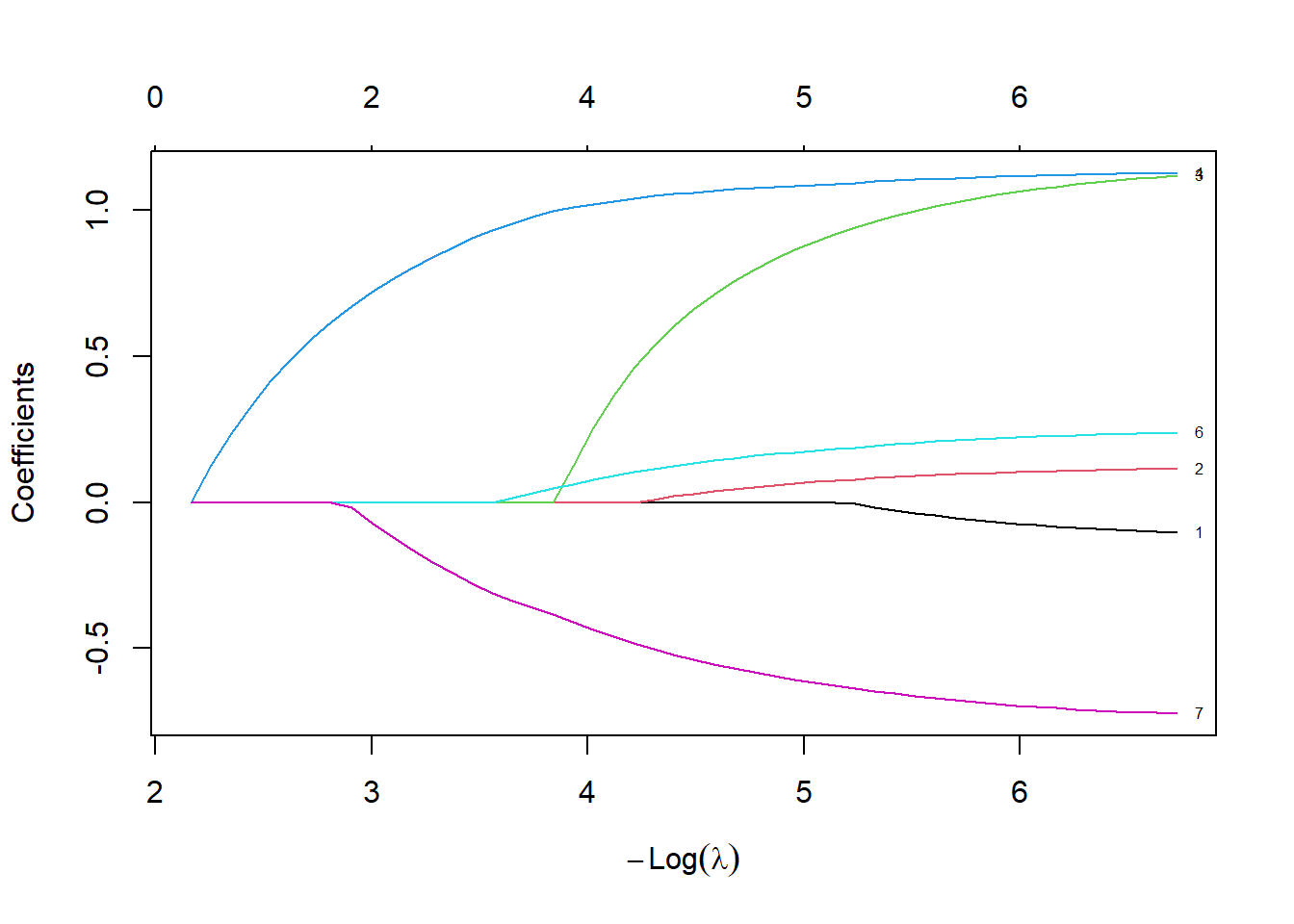

plot(lasso_fit, xvar="lambda", label=TRUE)

Let’s spend a bit of time looking at this graph. The left hand side of the graph represents a very small penalty.

fit_left <- as.matrix(coef(lasso_fit, min(lasso_fit$lambda)))

fit_left 1

cvd -0.1045003

afb 0.1151425

sho 1.1199680

chf 1.1288924

av3 0.0000000

miord 0.2387614

mitype -0.7244685plot(lasso_fit, xvar="lambda", label=TRUE)

text(

log(min(lasso_fit$lambda)),

fit_left,

unlist(dimnames(fit_left)[1]))

Notice how the coefficients are very close to the Cox regression model. There is very little shrinkage and only one variable, av3, are zeroed out, meaning that it is totally removed from the model.

fit_median <- as.matrix(coef(lasso_fit, median(lasso_fit$lambda)))

fit_median 1

cvd 0.00000000

afb 0.02505858

sho 0.63270940

chf 1.05928764

av3 0.00000000

miord 0.12988143

mitype -0.53060276plot(lasso_fit, xvar="lambda", label=TRUE)

text(

log(median(lasso_fit$lambda)),

fit_median,

unlist(dimnames(fit_median)[1]))

At the middle (median) value of lambda, several of the variables are zeroed out. Most other variables are shrunk towards zero, relative to the fit with the smallest value of lambda.

What happens at the largest value of lambda?

fit_right <- as.matrix(coef(lasso_fit, max(lasso_fit$lambda)))

fit_right 1

cvd 0

afb 0

sho 0

chf 0

av3 0

miord 0

mitype 0plot(lasso_fit, xvar="lambda", label=TRUE)

text(

log(max(lasso_fit$lambda)),

fit_right,

unlist(dimnames(fit_right)[1]))

Once lambda gets large enough, the penalty is so great that the algorithm zeroes out every single variable.

Cross-validation to select the optimal value of lambda

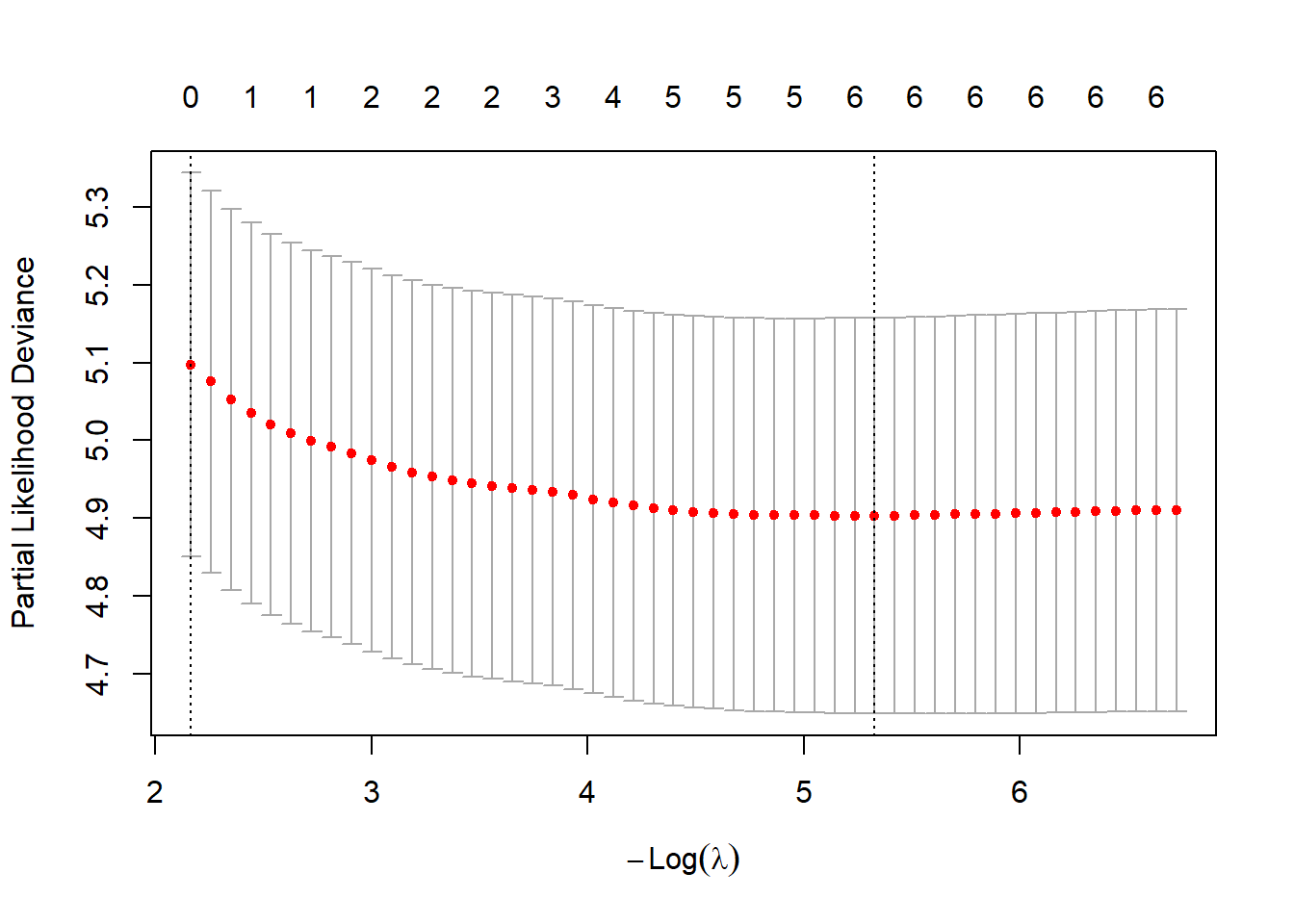

Now you need to decide what lambda works best. You can do this through cross-validation.

cv_fit <- cv.glmnet(xmat, ymat, family = "cox", standardize=FALSE)

plot(cv_fit)

There are two choices that are commonly selected.

You could set the value of lambda to the value that minimizes the criteria. The default criteria is the partial likelihood deviance, but you can use other criteria to pick out the “best” value of lambda.

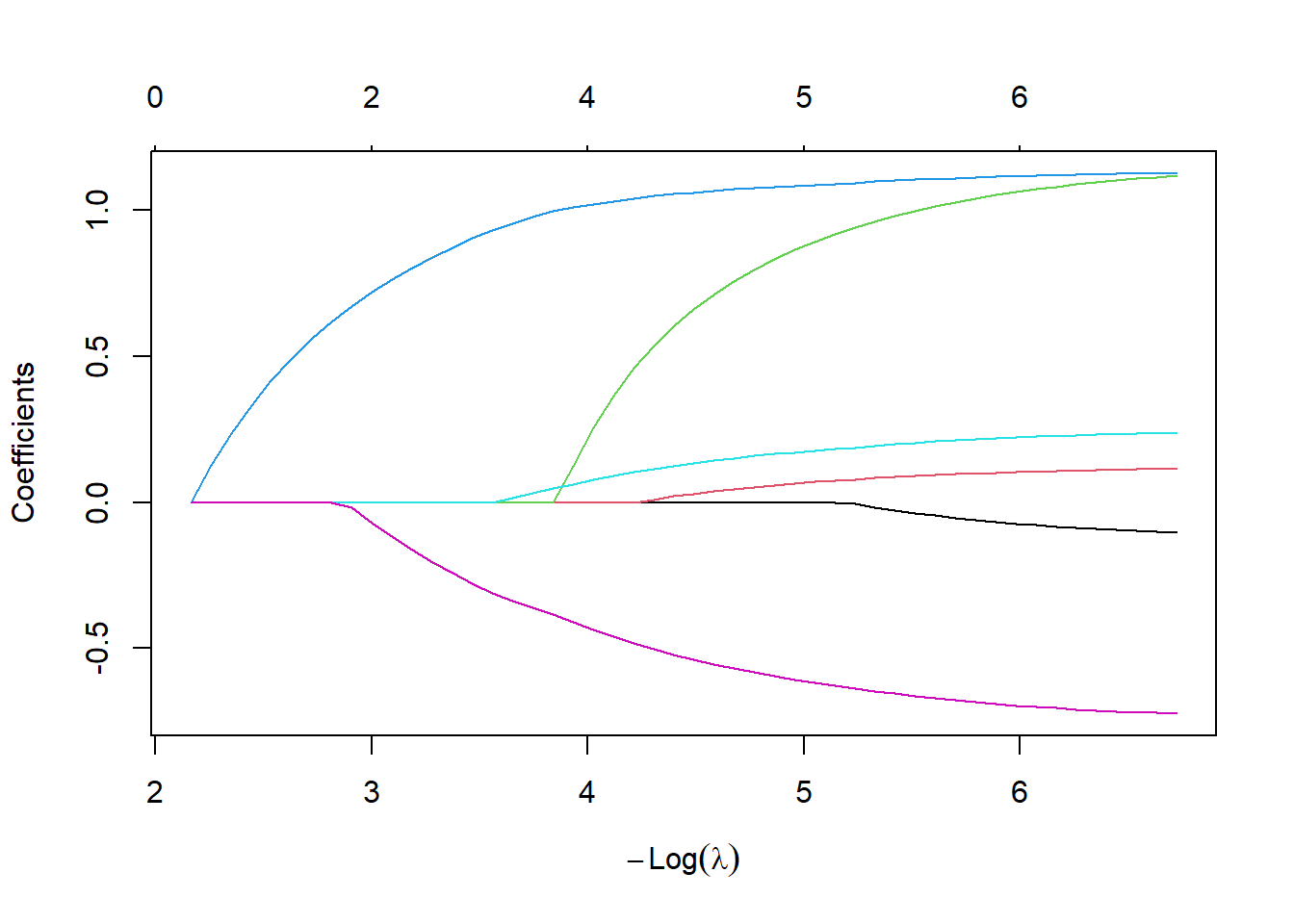

cv_fit$lambda.min[1] 0.004855224plot(lasso_fit, xvar="lambda")

abline(v=log(cv_fit$lambda.min))

fit_min <- as.matrix(coef(lasso_fit, cv_fit$lambda.min))

fit_min 1

cvd -0.01737968

afb 0.08333976

sho 0.96283217

chf 1.09896576

av3 0.00000000

miord 0.19388646

mitype -0.64692124text(log(cv_fit$lambda.min), fit_min, unlist(dimnames(fit_min)[1]))

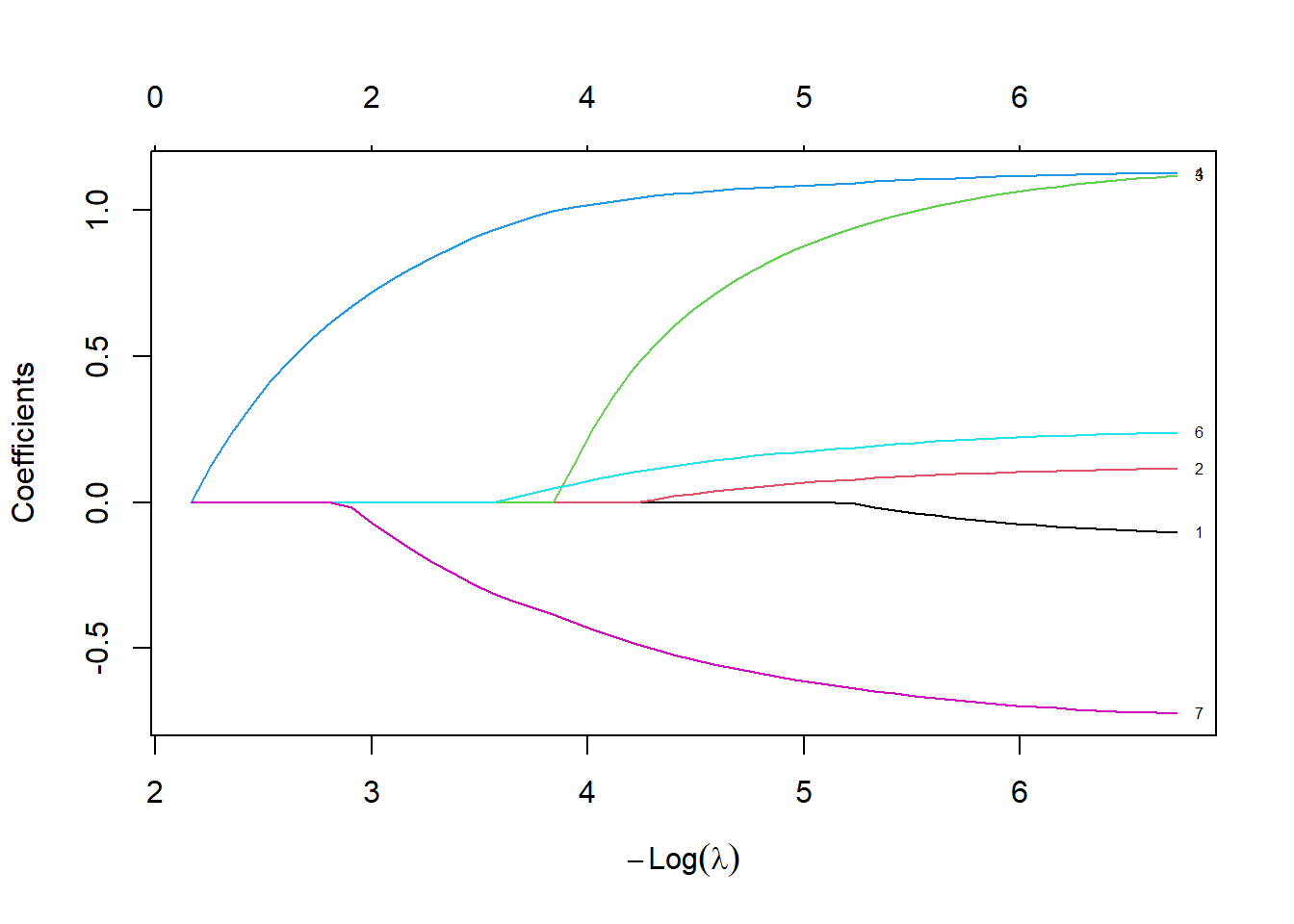

The developers of glmnet felt that the value of lambda that minimized a fit criteria was not aggressive enough in zeroing out and shrinking coefficients. They suggested that instead of choosing the “best” value of lambda, choose the largest value of lambda that is still within one standard error of the criteria produced by the “best” lambda.

plot(lasso_fit, xvar="lambda", label=TRUE)

abline(v=log(cv_fit$lambda.1se))

cv_fit$lambda.1se[1] 0.1148013fit_1se <- as.matrix(coef(lasso_fit, cv_fit$lambda.1se))

fit_1se 1

cvd 0

afb 0

sho 0

chf 0

av3 0

miord 0

mitype 0text(log(cv_fit$lambda.1se), fit_1se, unlist(dimnames(fit_1se)[1]))

Using this criteria, there are only two variables which help in predicting risk of death, and one of them is very weak because its coefficient is very close to zero.